Video: Remittances in the Pandemic Age – Obstacles and Opportunities

Continuing our recent spate of discussions exploring some of the challenges being faced by the remittance sector in the wake of the COVID-19 pandemic, RemitONE hosted a webinar on the 23rd June 2021 regarding the obstacles and opportunities of remittances in the pandemic age. The panel was made up of experts from both RemitONE and our friends and partners in other global companies. In case you missed the webinar, here is a summary of the key insights.

Webinar moderator:

- Aamer Abedi, CMO, RemitONE

Panellists:

- Leon Isaacs, CEO, DMA Global

- Naved Ashraf, Head of India & South Asia, MoneyGram International

- Julie Neogy, Managing Director: Global Payments, MFS Africa

Originally the World Bank predicted that global remittances were set to decline by 20% as a direct result of the pandemic. Was last year as bad as expected across the Middle East and Africa?

Leon Isaacs: The numbers probably indicate that it wasn’t as bad as had been forecast. If we think back to this time last year, things were generally looking pretty grim for the second quarter. But actually, during the rest of the year, things really recovered in most countries. There might have been a projection of a 20% fall for last year but the actual fall ended up being only about 1.6% on a global basis – much smaller than even the most optimistic projections that were happening this time last year. I think all the individual stories behind both businesses and senders and receivers of remittances will probably show you the challenges but there’s also a great level of optimism and resilience that seems to have carried into this year.

What have been the main challenges during this period and in your point of view, are we at where you think we should be in terms of recovery?

Julie Neogy: We’re a digital payments company so we’ve actually been positively affected by COVID. In fact, our transaction values during that period doubled! I don’t really have an answer for recovery because it’s been so successful for us, but our partners certainly faced some challenges. Some of the remittance companies that we work with weren’t equipped for digital payments, for example, so they really had some hard times adjusting. I think it’s also worth mentioning the regulators were traditionally a little resistant when it came to cross border payments, but they really adjusted quickly during this time by doing things like waving transaction fees, allowing for larger limits and even encouraging interoperability in the central African region. There were challenges but I felt like besides ourselves we had a lot of our partners really thrive in that time period.

Naved Ashraf: Honestly, during April and May last year it was like doomsday and we saw an abrupt business decline because of job losses, people holding back on remittances, sending lesser amounts back home, retail locations being shut and curfews across the globe. It also led to reversed migration with people moving back home and not really knowing how long they were going to be staying for and how long the COVID situation would last. However, recovery was faster than expected. Obviously, there was governmental support, so all of this also led to people sending money back home to their loved ones or friends that needed it. And, as Julie mentioned, digital was a huge help. Moneygram is a hybrid company, and people really woke up to digital during the pandemic and started sending more money, even in countries like India, which is the largest remittance market in the world. In fact, we’ve seen triple-digit growth in the last few months.

Do you have any comments on channel cannibalisation? And do you think there is enough data out there in the market that our audience can access?

Leon Isaacs: I think the short answer is no. Obviously, the shift to digital has become very pronounced thanks to COVID but with money transfer platforms, the definition of digital often means digital only needs to be at one end of the transaction. So we should take any numbers with a pinch of salt. Also, more than half of transactions still involve cash as the key part of the transaction. Cash is still a key part of transactions even if one end is digital. I think the shift towards digital has really started, which is good. But from a data perspective, I think we’re going to need surveys that are conducted by governments or international bodies.

Some businesses have thrived during the COVID period, what do you think their differentiators have been to insulate them?

Julie Neogy: I would say it’s their agility. Agile companies have thrived. As soon as COVID hit our partnership with Moneygram skyrocketed because they were really open to changing the way that they thought and worked. For the people in the informal market that had a traditional resistance to digital payments, that barrier is now gone as digital became more of a necessity for them. I also think the companies that benefited most were the ones already in the digital space and were already on the right side of regulations, so had less groundwork to do.

What notable shifts have you seen in the remittance sector? What do you think will stick in the long term and where do you see the industry headed?

Leon Isaacs: Digital is definitely here to stay; it’s the new normal. I think that means digital as a channel rather than just remittances. So it doesn’t just have to be remittances that are being pushed, it could be lots of other financial services. In most cases, I think it has demonstrated to people that there are alternatives that they can access that are actually quite easy to use and have many advantages that they presumed they couldn’t get before. So for instance you can now transfer money to much more remote places and the speed and the certainty is all there. But I think some of that will undoubtedly shift back after the pandemic. Historically, remittances have generally been viewed as a transactional business but I think that’s changing. One of the things we’ve really seen is that digitisation gives consumers a better understanding of the product and gives us a better understanding of the consumer. And finally, perhaps for all of us, COVID really brought the attention of policymakers and governments back to remittances. Because of this increased attention, companies are also more likely to keep their customers or attract new customers because of the improvements being suggested by the regulators. For me, that might be one of the best long term benefits.

What do you think these bigger players are doing, the established players in our industry, what steps are they taking to tap into the informal sector?

Naved Ashraf: In the south Asian market the informal sector used to be a big market but I wouldn’t say it’s the same now. The rise of organised remittances has really taken over, and I think the biggest players are into all the nooks and corners of the countries now. The people who used to rely on somebody delivering money to them has almost completely stopped.

Julie Neogy: It’s hard to say when I’m wearing my MFS Africa hat because we are only working with regulated entities. But what I can say is that when we’re talking about mobile money usage, we look at the number of users we are sending to on both the sending side and the receiving side. And the actual amount of people we are sending to on the receiving side has increased in all of the countries that we do business in.

Aamer Abedi: For me, it’s all about interoperability. In a receiving market like India or Zimbabwe, for example, the ability for money transfer solutions and mobile network operators to work together should help bring the untapped sector into the formal fold. Because the informal sector hardly uses mobile phones. But when they realise that cash can be transferred into a mobile digital wallet in some way, and this digital wallet can be used to send money to other mobile phone users, then you are strengthening our sector and bringing new customers into the formal fold.

Leon Isaacs: Interoperability definitely has become more important as it allows non-bank financial institutions to participate in mainstream financial services. So, for instance, we’ve seen a major increase in remittance software companies being able to credit bank accounts. If you can put together what systems exist now, then you can move money across different types of services where it needs to go and allow customers to access different types of products more quickly without building something yourself from scratch.

Is the usage of digital payment vs cash/physical methods, sustainable post Covid?

Julie Neogy: I want to say yes, but in Africa, the main barrier for using digital payments has always been trust. But there are a lot of other barriers, especially in certain African countries where cash-out fees are really high and wallet sizes are really small. Countries like Kenya and Uganda made adjustments during COVID. Now if they revert to the old ways and the cash-out fees go up or if send fees are reimplemented then it’s hard to say how sustainable it is. It really depends on how the regulators in the receiving countries are responding.

Has the bank account situation improved with the drive to go digital? Or are we in the same situation, as we’ve always been?

Leon Isaacs: We thought that more digitisation would help but from what I hear, it is not making a sufficient difference. There are still lots of companies that are having real difficulties getting accounts, particularly the newer technology companies. This is not just a UK or Europe issue either, it’s happening in most parts of the world. In a way, the discussion around it has moved from a business model where there were lots of concerns around the risks associated with digital into a discussion around cryptocurrency. I think what is concerning for me is that from a government level, things were really bad in 2012 and 2013 with many companies losing their accounts. Then things hit a plateau, and because they weren’t getting any worse, attention came off. But of course, things weren’t getting any better either. For me, the problem is not really solved and it’s only going to get solved if governments are prepared to take action, and I think governments are reluctant to take action particularly. It’s actually where digitisation should help because there’s much greater transparency and control, and the ability to identify people.

Naved Ashraf: From a South Asian perspective it is still harder for smaller players to get remittance bank accounts than it is for bigger players, but it is possible for smaller players to enter the mainstream. You just have to work a little harder than the rest.

If we have the technology, and we are proving that the technology is there, then why aren’t the governments and regulators doing more to put pressure on banks to help sustain the industry?

Leon Issacs: Ultimately, most banks want or need to deal in US dollars and to do that they need relations with big NY banks and these are the banks setting the standard. Because everybody wants to deal in US dollars at the moment, all countries are affected. This is not just an issue for money transfer platforms, but banks too, and the problem will not be resolved any time soon. There was talk about maybe remittance companies only dealing in euros rather than dollars to avoid that, but you can’t do that on a global basis.

What next then, in terms of opportunities that lie ahead for both traditional and digital MSBs post-pandemic?

Naved Ashraf: We touched upon bitcoin but bitcoins are not legal tenders yet, it’s quite popular but not legal. The central bank digital currencies are obviously blockchain-based and that is used to combat the growth of too many cryptocurrencies. But no bank as far as I know has banned the central bank digital currency. In terms of opportunities for both traditional and digital MSBs, I think blockchain that combats cryptocurrency growth could be the way forward but the biggest hurdle for blockchain adoption would be standardisation. There’s SWIFT which is like a standard that other agencies are also getting set up, and once that comes in I think it will bring in a lot of standardisation across the board. Also, we have to deal with the multiple layers of banks right now, and the lack of transparency at the moment of money. And obviously, we can’t forget about the customers, whatever apps and websites we are using right now they have to be more customer-friendly.

What does the future for the remittance business look like as we are witnessing more and more third-party open banking apps being launched?

Julie Neogy: Competition is fierce and I think what’s going to be exciting is that companies need to offer more than just a money transfer system. As more third-party apps are launched, remittance companies need to innovate with the customer’s best interests in mind in order to stay on top. Companies really need to stay at the cutting edge and come up with actual products instead of just conceptualising them.

Naved Ashraf: What I see is that there are two mediums of transfer. One is digital and one is traditional. I would say the end goal is the customer because everything has been done to make it faster, cheaper, easier and more convenient for the customer to receive their money. What will happen I think is that both mediums will have to learn to co-exist. Cash is here to stay.

Leon Isaacs: I agree that cash isn’t going away any time soon because very few specific markets in the region can operate using only digital payments right now. Ultimately, the majority of our users live in markets where cash usage is still quite high. I guess the question is, can you make a big enough business out of digital at the current time? It is very difficult to do digital-only. You have to find the right markets with the right remittance software and you need to have as many options as you can make work for you economically for consumers. Because at the end of the day, the consumer is going to use the service that works for them.

For more information or to request a free consultation with one of our money transfer specialists, please email marketing@remitone.com

Video: Better Together – Building a New Global Standard for the Remittance Ecosystem

Continuing our recent discussions exploring the challenges being faced by the remittance sector in the wake of the COVID-19 pandemic, RemitONE hosted a webinar on the 23rd of June 2021. The 90-minute conversation centred around the concept that in order to “build back better” after the pandemic, the money transfer sector needs to work together to create a new global standard. The panel was made up of experts from both RemitONE and our friends and partners in other global companies. In case you missed the webinar, here is a summary of the key insights.

Webinar moderator:

- Oussama Kseibati, RemitONE

Panellists:

- Hugo Cuevas-Mohr, CEO at Mohr World Consulting

- Sidharth Gautam, Head of Sales at AZA Finance

How significant is the remittance industry and who are the traditional and new players in the remittance ecosystem?”

Hugo Cuevas-Mohr: I’ll begin by defining what remittances actually are. The term remittance implies a family member sending money to other family members, for example. Remittances for the world bank, meanwhile, are only considered “worker remittances”, so the money transferred between family members is around 650 to 700 billion dollars per year of recorded remittances. On the world trading stage, of course, this number would not be extremely significant, but it is important to understand that this is higher than the investment from one country to another. It is also much higher than the aid that developing countries receive, so the significance is relative to different countries. In terms of significance, it varies depending on the development of the country. By comparing the remittance figure to GDP you can see that some countries are at 30% to 35% of their GDP, which is the case in Nepal and Haiti, for example. Interestingly, by contrast, big countries such as China and India will undoubtedly have high volume, however, there is less significance as the GDP is low. Another comparison is the population: if you divide remittances by the population of the country, then you can determine the significance of the remittance ecosystem based on each average individual in that country. Using this logic, Lebanon is number 1 in terms of significance, as it is a small country with a small population and a huge amount of money every year. This same principle can be applied to towns as well.

Sidharth Gautam: I completely agree with Hugo. In fact, in a few south sub-Saharan countries, remittance is essentially their backbone. There is a word developed by the World Bank called LMIC: “Low and Medium Income Countries.” Remittance is incredibly important for LMICs. Their entire country arguably depends on them.

Hugo Cuevas-Mohr: Adding to that point, remember that money goes to the lower fourth or the lower fifth of the economy. Remittances are also an important backbone for poor families in LMICs, therefore they are a really important “backbone” for them. Regardless of how those poor families spend the money, it doesn’t change the fact that they depend on remittances to survive. Indeed, sometimes 60 to 70% of a poor family’s income is primarily derived from remittances.

Who are the traditional and new players within that ecosystem, focusing on the traditional versus new and formal versus informal?

Hugo Cuevas-Mohr: It depends on a few things. In remittances, there’s always a sending market and a paying market. With regards to the pandemic, there was a small decrease in certain countries, particularly if they depended on Europe. However, if they depended on the United States you actually saw an increase, which was completely unexpected. The traditional sending players have always been agent-based, so brick and mortar operations were affected negatively in the early part of the pandemic as people couldn’t visit those agencies. As a result, every new digital player saw an increase. The more digital the payment; the higher the remittances would be, for example in Africa, mobile money companies saw an increase in sales during the pandemic due to the fact that remittances landed in mobile wallets. So we have seen transformation, however, I think it is too early to tell what will change and what will stay the same as traditional companies are evolving.

Oussama Kseibati: In the past, in traditional Asian markets cash has always been king. But over the past 10 years we have seen innovation being brought into the market and a move towards digital that has been hastened by the pandemic. I think as we get to the second and third generations that are more innately familiar with new technology, things are only going to get better.

How do you think we can enhance payments through successful partnerships and working together?

Sidharth Gautam: Partnerships are absolutely critical. No one organisation can facilitate change by itself; it has to be a concerted effort. We all have our core competencies, so the best practice should be to focus on these competencies and then align with partners who have a laser sharp focus in another particular area. AZA Finance is a firm believer in that, and our partnership with RemitONE is proof. It’s a natural combination of one plus one rather than automatic progression. That way you can start to create an ecosystem of consumers, brick and mortar agents, digital companies, aggregators (AZA) and technology, providers like RemitONE. All of these players have come together to give a seamless, end-to-end experience to the consumer. There is no point in reinventing the wheel but we have to drive meaningful and coordinated change at a global level over a sustained period of time to make it happen.

Hugo Cuevas-Mohr: Sidharth is right on the money. It maybe even as recently as a year and a half ago, partnerships in this space weren’t really stories but it’s booming now. You have to understand that traditional companies did everything on their own and always built their own systems, distribution, networks and compliance. But that’s the old way of doing things and for some companies, it can be difficult to break the habit. There are so many legacy remittance systems right now, and sometimes it might be best to just scrub the old system entirely, salt the earth and start with something fresh. Realise what you’re good at – the thing that makes you different, and work with partners to fill in the gaps. Also, remittance is one financial service and there are many other financial services the same customers need, so you have to integrate those services. Unless you want to do all of that yourself, which becomes rather complicated, it’s always better to partner with a company that has the right knowledge and resources. The new breed of digital banks are all being built on that more modular way of thinking.

How does one foster a good working partnership?

Hugo Cuevas-Mohr: In our industry, the important partnerships that we have is with the banking sector and sometimes we forget that. It’s been hard in some markets to build good banking relationships and now you’ve also got cryptocurrency and the new wave of digital banks to deal with too. You need to create that banking partnership to provide that flow of funds in the collecting and disbursement sites and if you are cross-border you’re also dealing with foreign exchange, so you need to be able to be very good at managing currencies. How that partnership is able to exist and survive is all about transparency; sitting down and being honest with each other – what you need, what you’re willing to provide and how that partnership is going to be organised.

Sidharth Gautam: We are the biggest non-bank currency provider in Africa and apart from Southeast Asia, Africa is one of the biggest remittance receiving markets in the world. So we get a lot of requests from small and medium-sized MTOs that want to expand into Africa but lack the knowledge and the data to do so. They don’t have those resources like the big larger MTOs where they can hire a market research team and that is where the partnership comes into play. So, not only do we give them an aggregator and last-mile liquidity but we also help them with Google Analytics, for example. I feel like marketing is where you explore the unexplored and it takes a partnership to the next level. That’s where long-term relationships get forged.

How can you sort a good partnership from a bad one?

Sidharth Gautam: It is very clear to me what my core competencies are and where I can leverage somebody else’s competency. It’s both a mix and a marriage between two equals and it has to be built on a common remittance platform for everybody. There are always going to be challenges. We are a regulated industry so you can’t just partner with anybody. You need to be very clear as to whether or not your partner is certified and that is the basis of any partnership in our business. Remittance is a very fragmented industry – the top three players have major market shares and yet every day you see new players coming up, primarily in the digital space where you can launch in the space of a few months. So there are lots of little guys scrambling for attention that might not be on the same page as you from a regulatory perspective. So do your research. What you also need to see is how potentially scalable that partnership is. For a successful partnership, it is important to understand not only your core competencies but what you want to achieve by having that partner on board and where you want to end up.

Oussama Kseibati: I agree. In fact, I’ve known companies in the past that have chosen certain providers they want to grow their business with but because they’ve used a certain tech provider it’s very hard for them to now uproot their whole business and take clients over to a system that they can scale. Again they’ve gone with someone who’s slightly smaller or built their own system and it causes more headaches further on down the line.

Hugo Cuevas-Mohr: Partnerships sometimes don’t work. And that’s fine. Sometimes I speak with companies and I have to be quite philosophical about it and say that sometimes it works and sometimes it doesn’t and you can’t really put a finger on why. Also, companies change and you have to be flexible to see where the market, takes you. Maybe you need to get rid of a partnership because you’re going in a different direction? So flexibility is something that you must have in this market. The pandemic has arguably made it even harder for everyone to plan for the long term, so you need flexibility about how you set up your structure. Flexibility is part of the game in everything we do these days. Even as people we need to be flexible enough to adjust to new ideas and new possibilities.

What are the developing trends in our ecosystem and what is RaaS?

Hugo Cuevas-Mohr: Remittance as a Service (RaaS) is so interesting because it has been such a long time coming. It is essentially an all-in-one solution that allows companies to launch money transfer software services from any particular geographic location. How does it work? Let’s say you have a good brand in Southeast Asia or in Africa and you want to do business in the UK. Maybe you can put your own brand in a product like an app or a mobile wallet and it is your image but using a third-party service. That’s the deal – I give you my brand and we do a partnership together, all those remittances come to me but to my client in the UK or in Europe, it’s the brand they’re interacting with. You’re behind the scenes. It’s really going to change the market. What all regulators want is better service and lower cost; a more compliant remittance system and this could definitely give them that.

How can remittance fix the gig economy, and how should we participate?

Sidharth Gautam: That is my favourite question so far! We are all are so used to hearing this word, “gig economy,” but what actually is it? Let’s talk stats. As of 2020, 1 in 10 people in the UK is employed by this “gig economy,” the equivalent figure in the US is around 8%. By 2024, one in four people, which is 40% of the workforce, will be in the gig economy and how can remittance solve the problem? Let me give you a real use case: An Uber driver in the UK gets paid directly into their bank account, which is fine, of course. Now, let’s shift this problem to Africa, or Tonga or some other nondescript, sub-Saharan country where almost one-third of the population doesn’t have a bank account. How do these Uber drivers get paid? That is where this whole idea of mobile money and digital wallets comes into play. That’s what the gig economy is doing and up until now either these people are getting left out or the bank charges are not transparent and it takes ages for these guys to get paid. In the US and the UK, you do a transfer today from the UK and it’s in the US account the next day. But for Africa, it can take a week. I mean, it depends on the intermediary bank that might have its own checks charges but also, in certain parts of Africa there is one soft currency for seven countries and the banks of those seven countries don’t talk with each other. That is where organisations like ours play such an important role in the gig economy, helping these people get the money, faster and quicker because that’s the way forward.

For more information or to request a free consultation with one of our money transfer specialists, please email marketing@remitone.com

RemitONE integrates with payment gateway Vyne

RemitONE, the leading global, technology and business services firm for the remittance world, today announces its integration with Vyne, the specialist account-to-account payments platform.

The deal gives RemitONE’s 100+ remittance clients instant access to Vyne’s payment solution, becoming the fastest, most cost-effective way for their customers including Payment Institutions (PIs) and Money Service Businesses (MSBs) to send remittances globally.

Vyne uses Open Banking to move money in real-time between bank accounts, bypassing long-established but now outdated card networks and their associated fees. Vyne’s single integration means RemitONE’s clients can access the benefits of Open Banking including more secure, cost-effective, faster payments. With transaction times cut from days to seconds, RemitONE’s clients’ customers can send money abroad quicker than ever.

Because Vyne allows customers to make payments directly from their own verified bank account, “know your customer” (KYC) checks and “Secure Customer Authentication” (SCA) fraud authentication can be carried out quickly and seamlessly, reducing friction and vastly improving the customer experience.

Aamer Abedi, Chief Marketing Officer at RemitONE, says: “RemitONE is always seeking the most innovative payment products for our clients. The technical ease of Vyne’s payments platform allows MSBs to get up and running quickly, and offer their customers an efficient, robust and cost-effective way to transfer money. 10% of our MSBs took the first steps to integrate with Vyne within two weeks of the integration going live, with more client MSBs wanting to take advantage of Vyne’s Open Banking Solution every day.”

Karl MacGregor, CEO at Vyne, says: “The international money transfer market is booming. Globalisation and the rise in digitalisation means there’s an increasing need to send money abroad as quickly, easily, and cost-effectively as possible. This integration combines the power of RemitONE’s renowned money transfer solution and global network, with the easy integration, instant settlement, and fraud resilience of Vyne’s payments platform. Together we are opening access to a new way to pay, allowing remittance businesses to offer the significant competitive advantage of safer transfers and more seamless customer experiences.”

Take advantage of the RemitONE and Vyne partnership by contacting marketing@remitone.com

About RemitONE

RemitONE is the leading provider of money transfer software solutions for banks, telcos, and money transfer operators (MTOs) worldwide. Organisations of all sizes use the RemitONE platform to run their remittance operations with ease and efficiency by reaching out to their customers via multiple channels including agent, online and mobile. For more information on RemitONE, please email marketing@remitone.com

AML and CFT Guide for Money Transfer Start-Ups

Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT), are terms mainly used in the financial and legal industries to describe the legal controls that require financial institutions and other regulated entities to prevent, detect, and report money laundering and terrorist financing activities.

Every regulated entity should have appropriate AML as well as CFT checks and controls in line with the regulatory framework of the jurisdiction where the entity operates from.

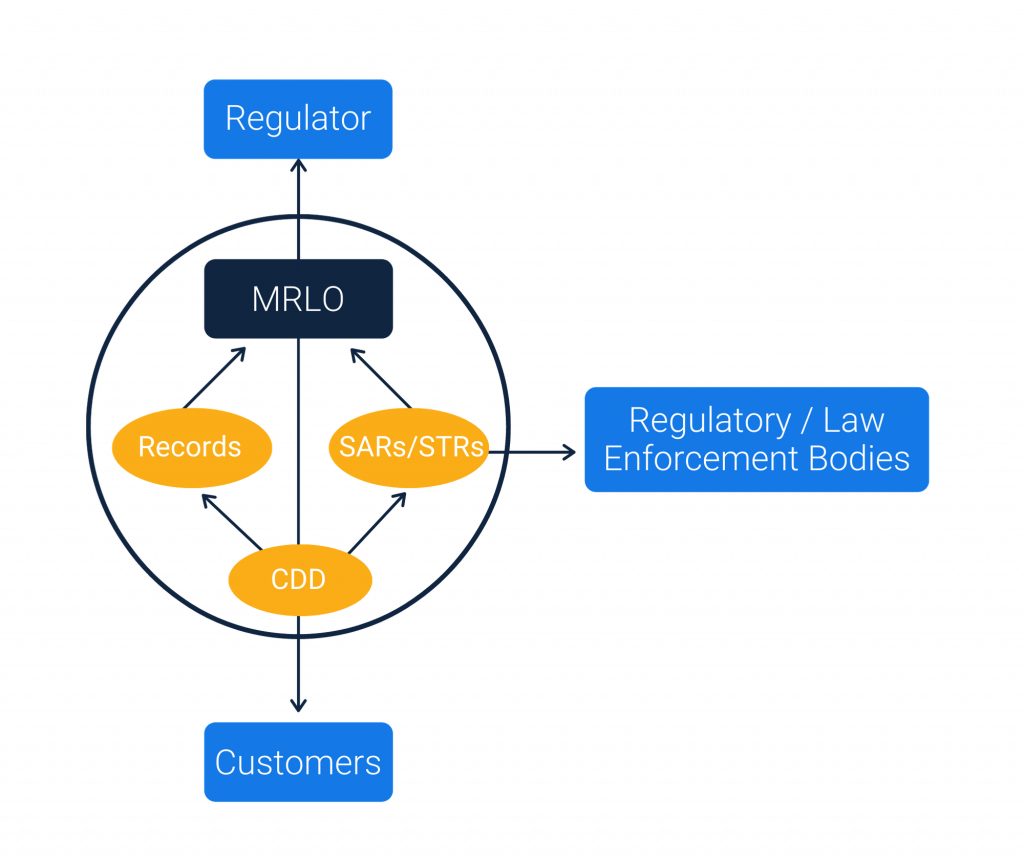

To make it easier for Start-Ups, please find below the diagram of the AML/CFT Ecosystem:

The ecosystem shown above shows the five core responsibilities of Money Transfer Start-Ups:

1. Onboard a Money Laundering Reporting Officer (MLRO)

First and foremost, all start-ups must have a dedicated Money Laundering Reporting Officer (MLRO) who is responsible for managing all compliance activities within the organisation. Depending upon the type and size of the business, there could be one or more members within the compliance team.

Aside from the MLRO, it is important that other stakeholders such as Directors, Senior Managers and even Shareholders familiarise themselves with the Payment Services and AML regulations within the jurisdiction where the business is registered.

2. Customer Due Diligence (CDD)

Each entity is responsible to identify the customers that they deal with. This step is known as the Know Your Customer (KYC). The MLRO has to identify the checks and controls that need to be in place to capture all the information needed from the customers as part of the KYC process.

Apart from KYC, the entity must also maintain the Customer Due Diligence which is mainly to do with checking the customers registering against the watch lists and the transaction patterns of the customers.

3. Suspicious Activity Reporting (SAR)

The entity is required to conduct appropriate investigations whenever an event such as a transaction monitoring alert or a sanctions match occurs. The MLRO has to validate such investigations further and need to report to the local regulatory bodies in the form of Suspicious Activity Reporting (SAR) or Suspicious Transaction Reporting (STR).

4. Record Keeping

The entity is responsible to maintain records of all their customers and transactions for a minimum period of 5 years or as per the guidelines of the local regulatory bodies. The MLRO has to ensure that the data captured from customers for identification and transaction purposes are stored securely and accessible to the authorized individuals of the entity whenever needed. Apart from customers and transactions data, the entity should also maintain the records of all the SARs/STRs.

5. Registering and Reporting to Regulators

The entity is responsible to have the registration done with the relevant regulatory bodies in the jurisdiction where the entity operates from. The entity should also be aware of all the reporting obligations in order to submit reports related to the customers or transactions data to the relevant regulatory bodies in the jurisdiction.

Whether you are a start-up or an established Money Service Business, it is very important that the AML policies and procedures are clearly incorporated within your business model. For more information, advice and support, please contact us.

RemitONE provides proven compliance products for Money Service Businesses and Central Banks and would be delighted to help your business. Contact marketing@remitone.com or call +44 (0) 208 099 5795.

RemitONE – AZA Partnership to Provide an End-to-End Money Transfer Solution

RemitONE, the leading provider of money transfer software solutions, announces its partnership with AZA, Africa’s largest non-bank currency broker.

This symbiotic partnership is a compelling proposition for money transfer operators sending money to Africa. Customers can now benefit from both RemitONE’s multi-channel money transfer platform and the ability to send money, airtime, bank transfers, and mobile transfers to Africa through AZA’s payout network.

AZA is a fully regulated Authorised payment institution by the FCA for the UK & Bank of Spain for Europe that specializes in both P2P & B2B last-mile payouts through its API solution across eight regions namely Nigeria, Ghana, Senegal, Uganda, Morocco, South Africa, UK and SEPA Region. It has immediate plans to expand to Côte d’Ivoire, Mali, Togo, Cameroon, DRC & Egypt within this year. AZA currently works with top-tier MTOs including Western Union, World Remit, Azimo, IDT (Boss Revolution), and is excited to add RemitONE to their list of partners.

“Our partnership with RemitONE takes us one step closer to simplifying cross-border payments in frontier markets,” says AZA CEO Elizabeth Rossiello. “Being a market maker, our focus has always been to offer the most competitive pricing to our customers and we are looking forward to serving more customers globally in partnership with RemitONE.”

RemitONE customers who are looking to take advantage of AZA’s competitive rates and payout network can easily integrate with AZA’s plug-and-play solution and gain access to these benefits immediately.

“We are very excited about this partnership, RemitONE and AZA are aligned on the core value of using technology to empower remittance and our aim to make it easy and cost-effective for people to send money home,” says RemitONE CEO Anwar H Saleem. “Our services complement each other and our partnership will ensure that we deliver a rich customer experience.”

Customers can benefit from both RemitONE’s highly successful and compliant money transfer platform as well as the ability to send money, airtime, banks transfer, and mobile transfers to Africa through AZA’s vast payout network.

Take advantage of the RemitONE and AZA partnership by contacting marketing@remitone.com

About AZA

AZA is an established provider of currency trading solutions that accelerate global access to frontier markets through an innovative infrastructure. By leveraging cutting-edge technology in their flagship products, TransferZero and BFX, they are able to significantly lower the cost and increase the speed of business payments to and from frontier markets. TransferZero is their B2B2C product, which provides both wholesale currency purchase and retail settlement via their robust API. BFX is their B2B over-the-counter platform for businesses with wholesale currency needs, especially those paying partners and suppliers. Their partners utilize AZA’s hybrid financial infrastructure and deep local knowledge to manage liquidity and send payments to dozens of bank networks and mobile money operators across Africa. They are licensed by the UK’s FCA and the Bank of Spain. For more information, visit: www.azafinance.com

About RemitONE

RemitONE is the leading provider of money transfer software solutions for banks, telcos, and money transfer operators (MTOs) worldwide. Organisations of all sizes use the RemitONE platform to run their remittance operations with ease and efficiency by reaching out to their customers via multiple channels including agent, online and mobile. For more information on RemitONE, please email marketing@remitone.com

Video: Remittances in Africa

Remittances: Getting digital-ready for post-pandemic recovery

The world bank has predicted that remittances are set to decline by 20% as a direct result of the pandemic, marking the sharpest decline in recent history. This is understandable on a surface level, of course, as remittance payments are most commonly sent between families and friends, and in the current climate, for migrant workers particularly, the pandemic has caused a dramatic fall in wages and employment.

However, the remittance sector is nothing if not resilient and for some, the pandemic has proven to be something of a catalyst for a sea of change that’s been simmering just under the surface for years now. Could COVID-19 be the final push the sector needs to jump off the digital cliff edge once and for all? With ‘Neobanks’ like Monzo, Starling and Revolut paving the way, the waters are not quite as untested as you might think.

Of course, our industry has various supply chain members, all of which will have a different opinion and angle on the story. As a leading technology vendor, we reached out to an aggregator (Sidharth Gautam from AZA Finance), a payment processor (David Lambert from Transact 365), an ID verification provider (Richard Spink from GBG) and a Money Transfer Operator, (Nadeem Quershi from USI Money), to ask them how they were preparing for a digital post-pandemic recovery and where they see the biggest innovations happening moving forward.

How do you see the future of the payments industry evolving?

Nadeem

The COVID crisis has had a profound impact on the escalation of digitisation in the payment industry. Our previous primary method of processing payments was rather manual, but in the wake of social distancing, we’ve been forced into ensuring our processes are more digitised. I think that’s going to have a major short and long term impact with digitisation continuing to escalate at a rapid pace.

Richard

It’s always going to be down to what the individual MTO wants to achieve when they run a compliance process. There’s a difference between just running a process and being compliant and our experience is that some businesses will want to take that seriously and others will want to just pay lip service to it. There are two reasons for that – one is that there’s a cost to being compliant and the other is that there’s a proliferation of vendors out there now. When I started in the UK 10 years ago there were perhaps 10 vendors. Now there are around 50 money transfer operators in the UK alone and hundreds globally.

How do you see the digital channel fees changing for MTOs as the channels shift from agents to a heavier reliance on digital channels?

David

The fees themselves always come down as volume goes up. When you’re talking about lower risk payment processing the margins are always going to be razor-thin. Already today I’m seeing fees online that are almost rock bottom and it’s only going to get slower. Then there’s the prospect of open banking which is going to blow everything open and remove the baseline costs even further. Ultimately it’s a competitive and a healthy environment and the fees are going to be falling but we are in this to help each other and make money. So while the fees might be coming down, we should always keep our shared end goals in mind.

Sidharth

70% of the remittance market today is cash-based but the tide is shifting and as it does the fees are going to go down. We’re already seeing it move southwards and as the 30% increases and the 70% reduces it’s going to exacerbate that reduction exponentially.

Richard

Prices will go down, of course. But they’re not going to suddenly plummet. There is a point at which we won’t go below (that rock-bottom David referred to) then there’s the cost of going digital that smaller MTOs have to consider. The price point will come down over time but then the technology you choose to invoke will change over time too.

The other thing that’s happening at the same time is that businesses are talking about digital ID. So the technologies to digitise identities is already there but the confidence to accept it probably isn’t just yet. In the next 12 months if you’re looking at how to make your process complaint online you have plenty of choices and the decision needs to be whether you’re looking for a quick fix or a process that’s scalable in the long term?

How does risk play into digitising money transfer?

Nadeem

The real question is do MTOs assume more risk online than in the traditional model? I believe that they don’t. We’re living in an age where digital risks have been largely mitigated by the complexity of new digital IDs. So I honestly don’t see it as any riskier than the traditional model of somebody visiting a brick and mortar location and presenting a physical ID. We have automated lists with regards to sanctions and screening so can build watertight systems to manage risks that are arguably just as proficient as the traditional model.

David

I partially agree with Nadeem. However, I’d argue that the moment you remove the cardholder from the equation in a physical capacity, the risk naturally increases. We can never be 100% sure on the surface if the cardholder who is making the transaction is the actual cardholder. Not if we can’t physically see them.

Where Nadeem is correct is in the responsibility of technology in ensuring those risks are reduced. If the tech is implemented correctly and the right controls are in place then there is going to be less risk. But fraudsters are very smart and they’re always getting smarter. I’ve worked in money transfer for a decade now and have seen so many different ways that fraudsters can behave – loopholes and tricks that technology can struggle to keep up with. The risks are manageable if you do it correctly but if you get it wrong then the risks can be ten times higher.

Sidharth

My response would be somewhere in between Nadeem and David’s. Our business is focused primarily on Africa and in that region, we’re seeing a lot of digital MTOs joining our platform, more and more every day. AI will definitely play a part in mitigating the risk but the risk is always going to be there. The question is how fast the technology can improve.

Richard

As soon as you’re online you’re introducing more risks, but the technology is there to mitigate the risk. As a rule of thumb, If it looks dodgy then it probably is. As long as you run a verifiable process online to mitigate those risks then it’s worth any cost. All online businesses must accept that fraud is part and parcel of the deal. As long as you accept that, go into it with your eyes open and put the right amount of resources behind it then it’s always going to be worth the risk.

Does the digital model present more opportunity for MTOs or are we operating in a saturated market?

Nadeem

The amount of MTOs that have gone digital in the last 9 months is probably more than in the last 9 years and COVID has played a major role in that. A lot of these conversions are not new entrants into the market but are existing MTOs that has been operating more traditionally and have been forced into the digital model.

David

There’s always an opportunity to be found in chaos. Throughout history, hundreds of companies have been forged in times of crisis. Disney was formed out of the 1929 depression, Microsoft came out of a major recession in the 70s and in 2008 it’s the banking crisis that kicked off Bitcoin and Fintech. The way that compliance has moved forward so fast in recent months has really spawned a rise in applications for electronic money licenses.

The implications of that are massive and have led to an environment where everybody wants to be a digital bank. It’s like when the Beatles came along and everybody wanted to be in a rock band. Now, thanks to the Monzos and Revoluts of the world, everybody wants to be involved in Fintech. This is perhaps why, now that we’re all in crisis mode, that so many MTOs are looking to upgrade their money licenses so they can perform different functions and expand into something more.

Sidharth

Asia and Africa are frontier emerging economies. Whilst the vaccine will be a reality in the western world it’s going to take a lot longer to filter into the emerging markets. Given that they are the primary markets for our industry it’s even more apparent that digital is the way to go. Because whilst the western world might be able to return to some semblance of normality sooner rather than later, the emerging markets that rely on remittance are still going to need to rely solely on digital.

Richard

In theory, as long as a financial service business has a steady platform, they can drive the business in any way they want. I think the difference is whether your focus is on driving transactions or taking the bolder step of becoming a fully regulated business. Revolut is a good example of a business that has spent all of its time and effort acquiring customers and are now embarking on the hard bit of actually becoming a proper bank.

I think that everyone would like to see an organisation do that successfully – pivot from a business that has a large number of customers into one that actually makes money from lending money. There’s an opportunity there to scale a business from an MTO into something that provides other financial services too.

Are we seeing MTOs evolve into these Neobanks or are we saying that the pie is quite big and each will have its own role within that pie?

Nadeem

We are seeing the more established MTOs move from conventional standard payments into things like e-money wallets and they are using this type of functionality as part of their wider growth plans. But generally, I think we will be seeing some form of consolidation amongst the larger MTOs. In the larger sense, the more established players have access to more resources so they will be the ones that will be moving forward.

David

Sometimes I feel like an outsider and sometimes it’s good to have that perspective where I’m not immersed deeply inside the money transfer sector. But I advise, consult and work with several different money transfer companies. One of the things that’s interesting that I see from my perspective is that everybody has their strengths and their positions within the market. If you look at companies like Small World, for example, they work with so many smaller MTOs to provide payouts and if you look at Azimo they rely on a number of different partners to help them get into certain parts of the world.

No one can do everything by themselves as one complete unit. So consolidation and licensing are interesting for me because every single MTO out there is trying to do something relatively unique. One company might be stronger in one area than another and by working together they can offer something more holistic and of greater quality overall. So I think consolidation should 100% be on the roadmap for everyone. My only fear about consolidation is that it actually shrinks the competitive element of any industry but I think that’s a little further down the line.

Sidharth

It’s already happening. Around two and a half months back WorldRemit acquired Sendwave for $500 million. This was a growth acquisition and it’s one of many floating around right now. There is also word on the grapevine that Western Union may buy Moneygram, which is one of the top three MTOs in the world.

David

Sidharth said something interesting about acquisition for growth rather than acquisition for revenue and I have seen that a lot in the payments industry. There is a huge amount of consolidation of payment service providers buying other payment service providers simply to grow because growth is so essential for a lot of MTOs, especially when we’re operating on such thin margins.

With all this technology at our disposal, why are we still having an issue with de-risking?

Richard

Since I started talking to MTOs in 2012, I’ll be honest, it’s not got any easier. The first question I ask people as a qualifying question is ‘have you got a bank account’. If they haven’t got a bank account then they’re wasting my time because I know they won’t be using our software until they get that bank account.

The big banks just won’t take the risk. It’s too much hassle and that’s a business banking problem anyway. They could easily take the risk if they choose to, it’s whether they have the resources to be able to deliver that and that’s where you’ve got the disruption coming. Can smaller banks take on that risk? Because in another sense they have less risk in it potentially going wrong.

Nadeem

De-risking has been going on for a number of years but at the end of the day, from a bank’s perspective, it comes down to purely to risk versus reward. For this reason, I don’t think you’re going to see a change in banks attitudes or habits when it comes to de-risking. David also correctly mentioned the rise of the Neobanks and some of these smaller challenger banks but they come with their own set of limitations.

What about regulators? Should the onus be on them to make sure that this continues to be a vibrant and healthy 600 billion dollar industry?

Nadeem

Regulators are there to create a framework, structure, processes and regulations. When it comes to safeguarding good practices, regulators are increasing some of these rules and regulations but can they force banks to actually support clients? I don’t think that’s their objective or their remit.

David

I don’t think it’s in the regulators best interests to push the banks, I think when a company becomes FCA regulated it has to be independent of the banks in some respect. Because, if the FCA and banks were in cahoots with each other it would be it much easier to operate but you’d also leave yourself much more open to fraud. If the two remain independent and they are independently scrutinised you have a sort of double lock system.

Sidharth

Regulators are becoming more and more progressive enablers to our industry. At least in my experience. In the UK and Europe, we have the example of open banking which is fuelling innovation and is also making the industry more compliant. All the stakeholders are becoming more and more transparent and it is helping to increase the credibility of the segments.

Africa and Asia are still very very fragmented. 54 countries with 54 different regulations. So they have a lot of catching up to do but then you can clearly see in Kenya, Uganda and Nigeria that things are moving at a very fast pace and regulators are moving likewise.

Finally, where do you think the biggest innovations will be moving forward?

David

A lot of innovation is happening right at our doorstep in the Fintech space. Payments is an ever-evolving industry. Every single day there’s a new payment method, a new way of doing things or a new market that can be exploited. Once blockchain technology has crossed over into the mainstream and people realise they can effectively move money as fast as they can send an email, that’s going to be the big breakthrough, that’s the innovation.

Nadeem

There is excitement around blockchain, digitisation of tokens and the ability to make payments instantaneously, of course. But there’s also innovation around digitised prints in terms of digital KYC and simplifying processes for consumers. I think simplification is going to be a key in terms of ensuring not only that funds are instantaneous but that the customer relationship does not simply finish at the point of collection or deposit.

Our thanks to David, Richard, Nadeem and Sidharth for their words and their time.

For more information or to speak to one of our experts please email marketing@remitone.com

AI: Empowering Fintech and Money Transfer Firms

From its humble start in the 1950s to the extensive uses now frequently seen across all industries, Artificial Intelligence (AI) has very clearly grown into one of the most innovative and game-changing technologies. It’s becoming increasingly evident that the role of AI, especially within financial services and the digital realm of remittances, has become crucial for providing improved services. Even over the last decade, AI has continued to evolve, reducing and even eliminating manual processes for the financial services sectors.

Machine Learning and Security

Enabled by predictive power, pattern recognition and enhanced communication functionality, AI is proving it has the potential to boost financial services and transform the way these services are delivered to customers. AI could empower Fintech firms to have more informed and bespoke products and services, internal process efficiencies, enhanced cyber-security and reduced risk.

For example, in the payments industry, AI is currently being used for sanctions screening and fraud prevention – a process underpinning money transfer organisations. Until recently, many organisations screened for sanctions by checking data stored in mass databases. Although this technique is routinely used by most financial services firms, in recent years we’ve seen that AI can be applied to this activity as well as other fraud prevention processes. Learning through experience, the AI technology can begin to better understand the backend data in order to search more quickly and efficiently, ultimately resulting in fewer false positive results.

The Future of AI: Improved End-User Experience

In the next few years, we predict that the financial services industry will certainly begin to see an increased use of AI surrounding security and compliance, as well as other backend processes. However, it is also becoming more evident that money transfer operators (MTOs) could soon be incorporating AI on their frontend applications (mobile apps and online portals) to enhance customer experience.

For example, we’ve already begun to see instances of machine-learning powered ‘chatbots’ offering 24/7 support and guidance to MTO customers. Using natural language processing, these chatbots – amongst other AI-driven voice-based services – will be able to understand queries and provide solutions, enhancing the overall end-user experience.

In addition to this, a less obvious area for AI use we could be seeing in the near future is for managing the rates and fees charged to remittance customers or end-users. By applying machine learning, MTOs could begin to make predictions based on a variety of factors (including existing data, patterns and even seasonal changes) in order to help customers set their rates and charges more effectively.

Where Will AI Go Now?

It’s clear to see that AI and machine learning are beginning to drive a wide range of processes, both within the digital remittance realm and beyond. The outcome of this increase in automation is the opportunity for many companies to work more precisely and efficiently than ever before.

As a result, we can confidently predict that the financial services industry will be seeing a lot more of AI driven technologies. But what would you like to see from the remittance industry going forward?

If you’d like more information about the power of AI within Fintech or would like to engage in a discussion about the future of machine learning, please get in touch at marketing@remitone.com

R1 Webinar: The Future of Remittances

Video: Remittances from the Gulf – The Impact of Covid-19 and Trends for 2021

During IMTC World 2020, RemitONE’s CMO, Aamer Abedi, moderated an engaging panel discussion on Remittances from the Gulf – The Impact of COVID and trends for 2021. During the panel he asked industry experts from the UAE, Saudi Arabia and Pakistan; how the market has been impacted; has COVID accelerated a digital transformation; and what’s the landscape for competition in your region.

Watch the full discussion here or read the highlights below:

How has your region been affected?

Osama Al Rahma, Advisor at Al Fardan Exchange and Vice Chairman of the Foreign Exchange & Remittance Group in UAE, commented that in the UAE there has been an unprecedented lockdown and control of the mobility of people has been restricted. He adds that it is unique that the workforce in the UAE is 90% ex-pats from over 200 nationalities and all are under the wage protection system. In terms of remittances, the service continued during the lockdown, the government recognised receiving countries are in severe need for the service and it’s thanks to authorities that permission could continue.

Khalid Al Zain, Head of Business Development at Bank Albilad in Saudi Arabia, commented that the Saudi Arabian Government has been investing in the private sector to keep their staff employed. He adds, there have been measures from the regulators including social distancing. Khalid notices that there is an impact but it’s not too much. Due to the support from the government and measures taken, such as social distancing, hygiene and increased security. He adds that despite COVID the number of employees is increasing and the workforce is in a good shape in Saudi Arabia.

How has the market been impacted?

Faisal Rashid is Head of Financial Institutions, International Banking & Home Remittance Business at Bank Alfalah in Pakistan, he explains that as Pakistan is predominantly a receiving country you would expect the country to be impacted significantly by COVID. However, he has found that from the GCC, where Pakistan receives its bulk of transactions, remittances have grown by 25%. He adds this is driven primarily by a 66% increase from Saudi Arabia and a 17% increase from the UAE. He believes this increase is due to the strength of partners in those regions moving from agent to digital channels. He also mentions that the receiving side in Pakistan has struggled to convert to digital pay-out due to the lack of infrastructure and the digital ecosystem.

Osama explains that in the UAE there have been declines in remittances, Egypt by 8%, India by 17% and the Philippines by 24%. However, they have seen growth in Pakistan by 11.5%. He believes this increase is due to transactions going through unofficial channels now moving to official channels. It could be argued that this is one of the positives coming out of the pandemic.

Khalid adds in Saudi Arabia they saw a decline in remittances during the initial phase of the pandemic, however, this has since changed and overall, they have witnessed growth in remittance by 8%. He also explains that customers are moving to digital channels rather than using traditional methods.

Has COVID accelerated a digital transformation?

Faisal comments that Pakistan is a young population who understands modern digital communication tools, however, only one-third of the total population is using smartphones causing a barrier to moving online. He adds that basic smartphones are now becoming available which is what Pakistan needs to create an ecosystem to make it easier to move money around. The graduation of moving to digital channels has started, all banks are working on their digital offering and we will see a large shift in the coming years with COVID hastening the transformation.

Osama agrees that COVID has accelerated the digital transformation of remittances in the UAE, but mentions that the Government of the UAE created a strategic initiative for digital transformation before COVID, which included strategy around infrastructure, policies, regulation and cybersecurity. This initiative includes the ‘UAE Pass’ which provides UAE citizens with full digital identity. These initiatives coupled with 80% of the population using smartphones, have provided the UAE with a seamless transition to moving online. Osama notices that the technology, infrastructure, and cybersecurity are all available in the country, which enhances the customers’ experience on the digital level.

Khalid has found that the migration of customers to digital is going excellently in Saudi Arabia and he notices a spike in migration of customers to digital. He explains that all citizens in Saudi Arabia are required to provide a fingerprint for their ID card and data has been stored in the mainframe. The private and government sectors can liberate from this data which has allowed Khalid and his team to introduce E-KYC seamlessly. Khalid notices that lots of customers are moving from traditional methods to digital.

What’s the landscape for competition in your region?

Khaled comments that Saudi Arabia wants to be a cashless society by 2030. He adds there are lots of strategies and initiatives in place, organised by the Saudi Arabian regulators, to open the market and invite many players to come. He believes that by increasing competition in the market, services will improve and it’s not just about one bank, there are lots of players in the market.

Similarly, Osama explains, in the UAE we have regulatory bodies such as Abu Dhabi Global Markets (ADGM) they have their regulations and initiatives for start-ups to support, facilitate and encourage fintech companies. The UAE also have Hub 71, which is a body to support start-ups, that have a payment lab to support innovation and testing. He adds, In Dubai, we have the Fintech Hive and the Dubai Economic Develop Department, where Pay Engage is the latest initiative. He explains that initiatives are being set up to allow for more innovation and similarly to Saudi Arabia, to move towards a cashless society. He concludes, there are strategies and clear milestones in place, with all stakeholders involved including federal and local government. There is a shift and it’s happening very quickly which is encouraging many companies to move their businesses to the UAE because they can benefit from the infrastructure.

Conclusion – COVID-19: An agent of change

The pervasive atmosphere in the sector appears to be one of defiant optimism in the face of some pretty sobering stats. The vast majority of the challenges posed by the pandemic, however, are either short-term by nature or have, in some of the cases outlined above, already been overcome.

Remittance will always represent a lifeline for developing countries and as technology adoption continues to penetrate every part of the globe, digital transformation is something that can’t be ignored any longer. Nobody is going to remember coronavirus as a ‘good thing’ but it could at least be recognised as an agent of change and change is often necessary, even if it feels a little intimidating at the time.

For more information or to speak to one of our experts please email marketing@remitone.com